As a first time homebuyer we know you have a lot of questions. Our team here at Sun American Mortgage knows this and wants to make the path to homeownership as simple as possible.

Thoroughly answering all your questions and walking you through each step is important to us. Today we are going to cover some of the most popular questions we get from first time home buyers and break it down to the basics for you!

How can I best prepare to apply for a mortgage and purchase a home?

To purchase your first home, you’ll need a good credit score and DTI (debt-to-income) ratio, steady job history, and a size-able chunk of cash saved up for a down payment.

Does one of these areas need some work? No worries! Our team is happy to help you make homeownership possible. We will work together to build a plan specific to your needs – whether it’s helping you build your credit up or saving up for a down payment – our team here at Sun American will be there every step of the way!

What is a DTI? How does it effect my qualifying for a mortgage?

A lower debt-to-income ratio will lower your credit score and mortgage rates.

What is a DTI? Debt to Income Ratio is a major factor lenders look at during the mortgage application process.

The amount of debt you have compared to how much money your household is bringing in each month, lets lenders know how much of a monthly mortgage payment you’ll be able to handle.

Depending on which loan program you qualify for, determines which percentage of DTI you’ll need. Currently for a Conventional and FHA loan program, you can get an approval at 50% DTI. Generally you should try and stay under 45%.

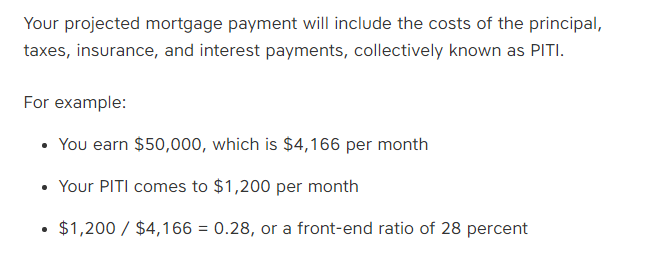

Below is an example from studentloanhero.com with a break down of how DTI or PITI works.

Click here to calculate your DTI!

How can I apply for a mortgage loan?

A simple loan application will collect things like your current income, assets and debts. The loan officer will then use this information to get you lined up with several different loan programs that will fit purchase price and monthly payment goals.

Here at Sun American Mortgage we have made applying for a mortgage easy, efficient, and right at your fingertips! You will receive updates throughout the entire process and you can upload documents with our Online Accelerator. Use our Online Accelerator here to start your mortgage application today!

Whether you apply for your mortgage loan in person or on your phone, our team will be thorough and walk you through each step of the way!

Between my husband and I, we have thousands of dollars in student loan debt to pay off. Does this affect us qualifying & purchasing a home?

Most mortgage lenders don’t mind student loan debt, as long as there is proof to show you are paying your monthly payments on time. It is still wise to pay off as much as you can before applying. But don’t sweat it if you have student loan debt on your shoulders. Almost everyone has some, what’s important is how well you make you’ve been making your monthly payments.

Our team of Loan Officers have helped many first time home buyers purchase their first home. One of our Loan Officers Derek Hargrove says this regarding student loan debt:

“Student loan debt is not the end of the world. Incurring that debt in order to gain some type of specialized training is generally viewed as a good investment that will pay off in the long run! Once the student has graduated and found a job they will normally take advantage of a “post-graduation deferment option”. This is where no payment is due on their student loans for 6 months after they have completed their last class. This deferment period can be kicked out, further pending student loan servicer approval and is not generally something that the servicer will fight you on. Interest is accruing on the debt and you are still obligated to pay it in the future, so the servicer is willing to defer the payment now for more money later. The former student generally plans to kick them back into repayment once they have gotten established in their industry and start making some good money. This is very budget friendly out of the gate but ends up wreaking havoc on a mortgage application as a mortgage company is required to use 1% of the deferred balance as a payment in the debt to income ratio.

For example, a $50,000 student loan debts digs a $500 per month hole in an applicant’s debt to income ratio and will severely limit their ability to qualify for a loan. However, current underwriting guidelines will allow a mortgage company to recognize income based repayments. The student loan servicer will require you to submit proof of income and adjust your required monthly payment accordingly. For example, a $50,000 student loan debt could be flipped from a deferred status that I would have to recognize as a $500 payment to a $20 per month income based repayment depending on your income. This $480 difference in the debt to income ratio calculation will completely change the application and allow you to qualify for way more home that you would have been able to qualify for previously. It is a complete game changer!!!”

We offer some great programs that would benefit first time home buyers with student loan debt, click here to learn more!

What is the difference between Pre-Approval and Pre-Qualification?

After you are pre-qualified, your Loan Officer is able to prepare an accurate pre-approval letter. This is used most often when purchasing a home. The letter is then given to your represented real estate agent as well as to the sellers agent, which ensure you are qualified to purchase the home you’re about to make contract on.

The seller’s agent will oftentimes call the loan officer to see how solid your pre-qualification is. This gives us a great opportunity to brag about awesome you are and convince the seller to accept your offer!

Once your real estate agent has been able to help you go under contract on a home they will send your loan officer a copy of the contract so that the real fun can begin!

Which loan program do I fall under?

For first time home buyers there are a lot of different mortgage loans out there to choose from – so how do you decide which is right for you? It’s important to thoroughly research each type of mortgage loan program and understand the benefits of the different financing options available to you!

As you are going through the mortgage application process, your Loan Officer will help decide which loan program will fit your needs best. Click here to learn all about the loan programs we offer and their qualifications!

I don’t currently have any established credit. How can I start building it up now so that I may qualify for a home soon?

Derek, our loan officer here at Sun American offered this great credit building tip for first time home buyers: “Establishing credit can be tough for people. It is hard to find a bank that is willing to give you a chance if you don’t have any history but it is impossible to get any history if a bank won’t give you a chance. This conundrum has a very simple solution that I would be happy to walk you through.

Here is what I would do to get established. It is easy, simple and can be set in motion with about an hours’ worth of work. You need a secured credit card. There are a ton of banks out there that will set up a secured credit card and essentially allow you to borrow money from yourself. For example, let’s say you walk into a bank with $500 cash. You tell the teller that you want to set up a secured credit card. They have you sit down with an adviser. The adviser takes the $500 and puts into an account as collateral against your new line of credit. The new line of credit will have a $500 limit and will have a normal looking credit card that you can use like any other.

You start to you use the card responsibly and pay down the balance regularly. The bank gets to report that good behavior to the credit bureaus and your credit score goes through the roof within a few months. The bank has next to no risk in this line of credit and generally will not even require a credit check because you are effectively borrowing that money from yourself. Once you have a credit score you can apply for other more traditional lines of credit that do not require a deposit or secured account. After a few months of this even a person with a completely non-existent credit score will be well within range of being able to purchase a home. I have seen it happen lots and lots of times before. It works like a charm!”

First Time Home Buyers Experience With Us

We know purchasing a new home is a big step and for many, a brand new chapter in life! We take pride in making this the most memorable and positive experience for you, walking you through every step of the way!

Here are some of our recent testimonials from first time home buyers and their experience working with us:

Let’s Get Started!

Now that you see how easy it is to qualify- what are you waiting for?! These affordable programs are right at your fingertips and just an application away. Our team of experts have the best programs and love helping home buyers qualify for their new dream home, or refinance their existing one.

Click here to meet our team and get started today! Call us to get a quick estimate at 480-832-4343

Below are some of our past blogs that will also help guide you on your path to becoming a homeowner! We hope all your questions have been answered. If we missed any, please contact our team at 480-832-4343 and we would be happy to help!

4 Things That Don’t Matter When You’re Choosing Your First Home

Simple Savings Tips To Save Up For Your Dream Home In a Year!

How The Mortgage Process Works

5 Benefits of Becoming a Homeowner

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}